The 2025 federal tax changes (commonly called the “One, Big, Beautiful Bill” or OBBBA) brought sweeping modifications to deductions, credits, and business expensing. While these changes were enacted at the federal level, states decide independently whether — and how — to “conform” to federal tax law. That means some states adopted certain provisions, some selectively adopted them, and others explicitly decoupled to protect state revenues.

This guide is a state conformity tracker: it explains how conformity works, summarizes which states have adopted or rejected major 2025 federal changes (with links to official guidance), and offers practical advice for taxpayers and businesses.

WHY STATE CONFORMITY MATTERS?

When a state “conforms” to the Internal Revenue Code (IRC), it typically uses federal definitions (often based on a specific date) to compute state taxable income. But states can:

- Adopt the IRC as of a certain date (rolling or fixed conformity), or

- Pick-and-choose (selective conformity), or

- Decouple (reject certain federal provisions and require add-backs).

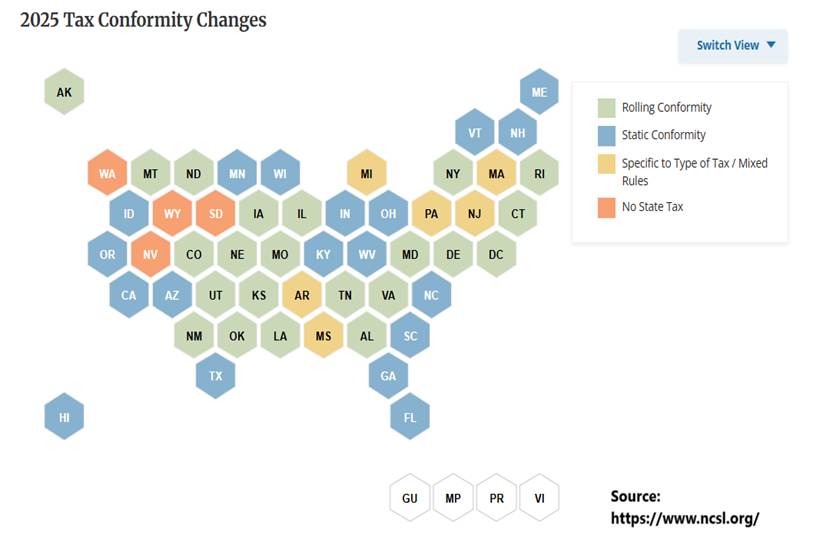

Because the Tax Year 2025 law reintroduced large federal incentives — especially 100% bonus depreciation (168), restored immediate R&D expense (Section 174 changes), and worker-focused deductions (tips/overtime) states faced potentially large revenue losses. Many reacted by decoupling from some or all of those provisions. The National Conference of State Legislatures (NCSL) provides an ongoing summary of state conformity actions that can be viewed here: https://www.ncsl.org/fiscal/2025-tax-conformity-changes

MAJOR NATIONAL TRENDS (WHAT MOST STATES ARE DOING)

- Bonus depreciation & R&D expense: Many states have long chosen not to follow federal bonus depreciation rules. Some states fully disallow bonus depreciation. Others allow it only after taxpayers add it back and deduct it over time. For Tax Season 2026, those states largely kept the same position. They did not adopt the restored and expanded federal bonus depreciation. They continued to require add-backs instead. The same pattern applied to federal R&D expensing changes. Several states required taxpayers to add back R&D expenses rather than deduct them immediately. See the Tax Foundation’s state-by-state analysis to understand which state adopts or decouple. https://taxfoundation.org/wp-content/uploads/2025/07/OBBBA-State-Conformity-Handout.pdf

| State | Tax Year 2025 Conformity | What Changed / Key Impact | Authoritative Reference |

| California | Selective conformity | Advanced IRC date to Jan. 1, 2025, but excluded major OBBBA provisions. Many federal incentives do not flow through automatically. | California Franchise Tax Board – Schedule CA Instructions |

| New York | Add-backs required | Continues separate depreciation calculations and requires adjustments for accelerated depreciation. | NY Form IT-399 & Instructions |

| Illinois | Legislative decoupling | Enacted statutory decoupling from federal bonus depreciation and related provisions. | Illinois FY-2025 Legislative Summary |

| Michigan | Add-backs via forms | Updated individual and corporate forms to adjust for decoupled bonus depreciation and other federal changes. | Michigan TY2025 Forms & Guidance |

| Delaware | Partial conformity | Picks up the federal SALT cap increase but does not adopt certain worker-focused deductions (tips/overtime). | Delaware Division of Revenue Notices |

| Rhode Island | Targeted decoupling | Limits bonus depreciation and/or R&D expensing; add-backs required. | Link at the end of the table |

| Maryland | Targeted decoupling | Does not fully adopt federal bonus depreciation or immediate R&D expensing. | Link at the end of the table |

| New Jersey | Targeted decoupling | Maintains separate depreciation and expense timing rules. | Link at the end of the table |

| Connecticut | Targeted decoupling | Requires add-backs for certain federal incentives. | Link at the end of the table |

| Massachusetts | Targeted decoupling | Selective conformity limits accelerated depreciation benefits. | Link at the end of the table |

| Minnesota | Targeted decoupling | Uses fixed conformity date; requires adjustments for newer federal provisions. | Link at the end of the table |

| Pennsylvania | Targeted decoupling | Does not follow federal bonus depreciation; state adjustments required. | Link at the end of the table |

| District of Columbia | Explicit decoupling | Rejected certain OBBBA worker benefits, including no-tax tips and overtime; revenue redirected to local programs. | D.C. Office of Tax and Revenue |

- SALT (State and local tax deduction): A handful of states adjusted administrative guidance to reflect the federal SALT cap increase for 2025, but state-level treatment varies greatly. The following link provides information on state-by-state OBBBA conformity. https://taxfoundation.org/research/all/state/big-beautiful-bill-state-tax-impact

- Worker deductions (tips/overtime): A few jurisdictions (notably the District of Columbia) explicitly rejected or limited the federal “no tax on tips” / “no tax on overtime” provisions to preserve revenue or to fund alternate state programs.

STATE-BY-STATE SNAPSHOT

Below are states that took prominent actions to decouple, modify, or otherwise respond to 2025 federal changes. For each state, we include the authoritative link you can direct clients to.

Aggregated for remaining State: https://taxfoundation.org/research/all/state/big-beautiful-bill-state-tax-impact

HOW THIS AFFECTS TAXPAYERS — PRACTICAL EXAMPLES

- Small business buys a $200,000 piece of equipment in 2025. Federally, 100% bonus depreciation may allow a full expense in 2025 — but if your state decoupled (e.g., California, Illinois), you’ll need to add back the bonus depreciation on the state return, increasing state taxable income. That may reduce the federal cash-tax benefit at the state level.

- Retiree benefitting from the temporary senior deduction (extra $6,000): Some states (including D.C.) chose not to pick up the senior bonus deduction — meaning the retiree may pay more state tax despite lower federal tax.

- Gig worker and 1099-K changes: The IRS reinstated the $20,000/200-transactions threshold for Form 1099‑K reporting under OBBBA, but some states used different thresholds or retained prior reporting rules — keep careful records and check both federal and state guidance. IRS FAQs: https://www.irs.gov/newsroom/irs-issues-faqs-on-form-1099-k-threshold-under-the-one-big-beautiful-bill-dollar-limit-reverts-to-20000.

State conformity timelines — what to watch for

States may update their tax code at any time — some will pass quick “decoupling” bills in reaction to revenue estimates; others will adopt gradual or rolling conformity. The NCSL and Tax Foundation maintain trackers and summaries that are updated frequently. https://www.ncsl.org/fiscal/2025-tax-conformity-changes.

Where to find authoritative, state-specific guidance (quick links)

- National Conference of State Legislatures — State conformity changes: https://www.ncsl.org/fiscal/2025-tax-conformity-changes.

- Tax Foundation — OBBBA state tax impact: https://taxfoundation.org/research/all/state/big-beautiful-bill-state-tax-impact/.

- California FTB — Schedule CA instructions & conformity notes: https://www.ftb.ca.gov/forms/2025/2025-540-ca-instructions.html.

- Delaware Division of Revenue — tax season updates: https://revenue.delaware.gov/tax-season-updates/.

- Illinois FY-2025 Legislative Summary (decoupling): https://www.tax.illinois.gov/content/dam/soi/en/web/tax/research/legalinformation/documents/fy-2025-legislative-summary.pdf.

- IRS — One, Big, Beautiful Bill resources: https://www.irs.gov/newsroom/one-big-beautiful-bill-provisions.

IRS AUDIT GROUP

IRS Audit Group consists of tax professionals, CPAs, enrolled agents, and tax attorneys. We are located in Los Angeles, California, and our primary area of expertise is IRS Tax Audit Representation. However, our certified professionals cooperate and work with all IRS offices nationwide. Please get in touch with us for more information.

Telephone Number: (310) 498-7508

info@irs-audit-group.com